Tax policy is never just about numbers. It reflects priorities — economic, demographic, and political.

In 2025, federal tax law introduced a substantial expansion of deductions for Americans age 65 and older. On the surface, it appears straightforward: seniors receive additional tax relief. But beneath that headline lies a deeper structural question:

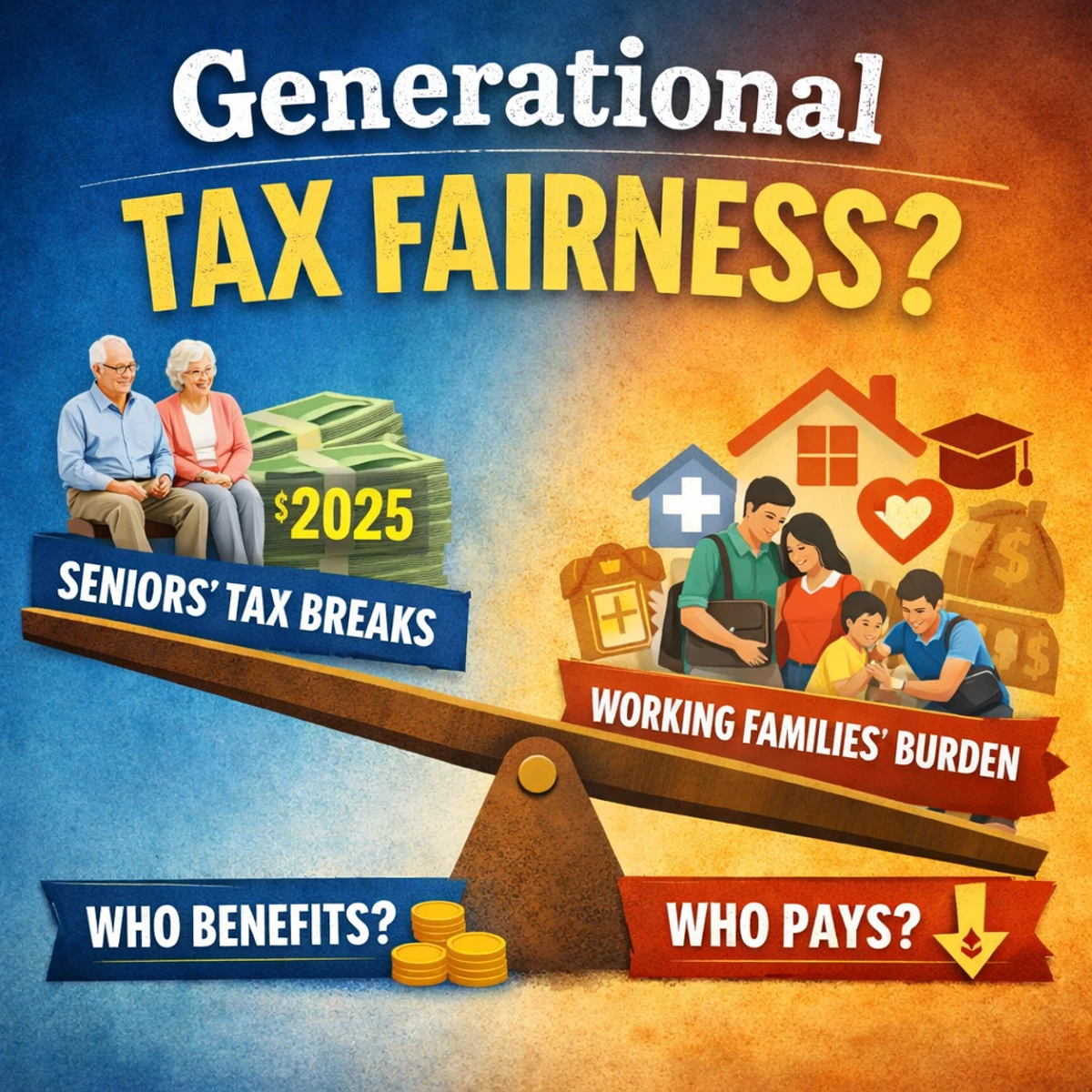

Who benefits most from this change — and how does it affect other generations?

This post breaks down the mechanics, distributional impact, and intergenerational implications of the 2025 senior deduction expansion.

1️⃣ What Changed in 2025?

Beginning in tax year 2025, eligible taxpayers age 65 and older can claim a new senior bonus deduction of up to:

- $6,000 per qualifying individual

- $12,000 for married couples if both spouses are 65+

This is layered on top of:

- The base standard deduction

- The long-standing age-65 additional standard deduction

What This Looks Like in Practice

For a married couple filing jointly:

| Year | Total Deduction (Both 65+) |

|---|---|

| 2024 | ~$32,400 |

| 2025 | ~$46,700 |

That is a $14,300 increase, or roughly a 44% jump in total deduction capacity.

By contrast, married couples under age 65 saw only an inflation adjustment:

| Year | Total Deduction (Under 65) |

|---|---|

| 2024 | $29,200 |

| 2025 | $31,500 |

That is a 7.9% increase, reflecting routine inflation indexing.

The proportional increase for 65+ households was more than five times larger.

2️⃣ Important Technical Clarification: Social Security Taxation Did Not Change

A key point of confusion:

The 2025 deduction expansion did not change the formula that determines how much Social Security is taxable.

- Social Security inclusion thresholds remain the same.

- The percentage of benefits included (0%, 50%, 85%) is unchanged.

- The deduction reduces taxable income, not adjusted gross income (AGI).

So the policy reduces taxes owed, but it does not change how Social Security benefits are calculated for inclusion.

This distinction matters.

3️⃣ Who Benefits Most?

Because this is a deduction — not a refundable credit — the benefit depends on:

- Income level

- Filing status

- Marginal tax bracket

- Whether the taxpayer already owes federal income tax

Most Likely Primary Beneficiaries

- Married couples age 65–74

- Middle to upper-middle income retirees

- Households with IRA withdrawals or pension income

- Taxpayers in the 12%–22% brackets

Who Benefits Less

- Low-income seniors already below taxable thresholds

- Seniors whose income is almost entirely Social Security

- Very high-income retirees above phase-out levels

- Working-age households (no direct benefit)

The largest dollar and percentage benefit is concentrated in the middle-income retiree cohort.

4️⃣ What About Working Families?

Working-age households face a different economic reality:

- Payroll taxes on every paycheck (Social Security + Medicare)

- Rising healthcare premiums

- Housing affordability constraints

- Childcare costs

- Student debt burdens

- Delayed family formation

Meanwhile, the standard deduction for under-65 households rose only with inflation.

This creates a visible asymmetry:

- Age-based relief expanded significantly.

- Working-age relief did not expand materially.

The structural tension isn’t emotional — it’s demographic.

5️⃣ The Demographic Context

The United States is aging.

- The 65+ population is growing rapidly.

- The worker-to-retiree ratio has fallen significantly over decades.

- Social Security, Medicare, and interest on the debt dominate federal spending growth.

Older Americans also vote at higher rates than younger cohorts.

In democracies, policy attention often aligns with turnout patterns.

That’s not unique to this policy — it’s a long-running structural feature.

6️⃣ Is This “Unfair”?

Fairness depends on the framework used.

Vertical Equity (Ability to Pay)

The deduction is not strongly progressive.

Higher-income seniors benefit more in dollar terms.

Horizontal Equity

A 64-year-old and a 65-year-old with identical income receive different treatment.

Lifecycle Equity

One could argue seniors face higher healthcare costs and fixed-income pressures.

Intergenerational Equity

If deficit-financed, the cost shifts forward to younger and future taxpayers.

Each lens produces a different answer.

7️⃣ The Fiscal Layer

If the expanded senior deduction reduces federal revenue without offsetting cuts or increases elsewhere:

- The deficit rises.

- Borrowing increases.

- Future taxpayers carry the financing burden.

That is not a moral claim — it is arithmetic.

The policy provides immediate relief but does not structurally reform Social Security taxation or entitlement spending.

8️⃣ What This Policy Does Not Do

It does not:

- Reform Social Security solvency

- Address healthcare cost growth

- Increase housing supply

- Reduce childcare costs

- Reform payroll taxes

It is targeted tax relief — not structural reform.

9️⃣ The Bigger Question

The deeper issue is not whether seniors deserve relief.

It is whether tax policy should prioritize:

- Age-based support

- Income-based redistribution

- Pro-growth structural reform

- Or generational rebalancing

In an aging society with slower population growth, these choices become more consequential.

Conclusion: A Policy Choice Reflecting Priorities

The 2025 senior deduction represents a significant expansion of tax relief for Americans over 65. It meaningfully reduces taxable income for middle-income retirees and delivers visible relief to a high-turnout demographic.

At the same time, working families — facing housing, healthcare, and childcare pressures — received only inflation adjustments.

Whether this is fair depends on your framework:

- Rewarding lifetime contributors

- Supporting politically engaged voters

- Managing short-term fiscal optics

- Or investing in future generational stability

Tax policy ultimately reflects priorities.

The question is not whether this change helps seniors — it clearly does.

The question is what it signals about how we balance generational responsibilities in an aging economy.

Back to Generational Economics